Table of Content

I recently refinanced my primary residence and took out a HELOC through Lower. Throughout the entire process Scott kept me informed with updates, was extremely responsive and very professional. The process went quicker than I expected and Logan was up to date on all steps of the process. I would recommend him to anyone buying or refinancing.

Standard guidelines might require a maximum 85% LTV ratio, but if you’re looking to borrow up to a 100% LTV home equity loan, take the time to shop around. You may be able to find the loan you need, just be prepared to pay higher interest rates. Home equity loan rates are typically higher than first mortgage rates. That’s because first mortgage lenders take priority over home equity lenders when mortgage debt is repaid in a foreclosure sale. Home equity rates can go even higher if you’re looking for a 100% LTV loan.

Home Equity (100 Ltv)

The more equity you have, the better your chances are of qualifying for a home equity loan. Your best bet for improving your LTV is to pay down your mortgage balance as quickly as you can. Another option is to dive into some home improvements that will bump up your home’s value.

Tap into the equity of your home to consolidate high-interest debt, fund a home improvement project, and more. Choose from a Home Equity Loan or a Home Equity Line of Credit. Below is an example of an LTV calculation for a homeowner with that same $400,000 house and $300,000 loan balance. Jared did an amazing job consolidating all of our debt and putting us into a great loan!

24% APR*

A GOOD CREDIT SCORE At a minimum, you’ll likely need a 620 credit score to get a home equity loan. But, to access lower interest rates, you’ll want a score of 740 or higher. However, each lender is free to set its own requirements, and may set a higher credit minimum for high LTV loans. Most HELOCs have adjustable rates, meaning they go up and down over time. Typically, the interest rate will be based on an index rate plus a personalized markup that is based on factors like credit score and debt obligations. If you’re perceived as a low-risk borrower, your rate will be lower.

Rates accurate as of December 9, 2022 and are subject to change throughout the day. All mortgage rates include Extra Credit Discount. OCCU Home Equity Loans offer great rates, five- to 20-year terms and loans up to 95 percent of your home’s value. If you’re considering tapping your home equity to access cash, here are some of the top lenders for a home equity line of credit . If your existing LTV ratio is above 85%, you can be considered a high-LTV borrower. If you are looking to secure a home equity line of credit 95 LTV then you have come to the right place.

What if you don’t qualify?

Keep in mind that home equity loan closing costs typically range from 2% to 5% of your loan amount. The short answer is yes, you can get a high-LTV home equity loan. Your LTV ratio represents the percentage of your home’s value being financed by a first and/or second mortgage.

You are being redirected...Javascript is required. Please enable javascript before you are allowed to see this page. Liberty FCU mortgage lending product availability may vary based on property location. Additional information may be required such as Divorce decree and/or proof of extra income such as rental income, dividends, Social Security, retirement, disability, pension, or welfare . Alimony, child support or separate maintenance documentation if you wish to have it considered as basis for repaying this obligation.

Home Equity Line of Credit (HELOC) – Canopy Credit Union

HELOCs are not available for secondary or investment properties. With HELOC loans from UFirst Credit Union, you can borrow up to 95% of your home's value up to $250,000. Borrow up to 80.01–100% of the equity in your home. Your savings federally insured to at least $250,000 and backed by the full faith and credit of the United States Government.

Generally speaking, IRS rules allow you to deduct the interest paid on mortgages used to “buy, build or improve” a home, including home equity loans, worth up to $750,000. Your home is being used as collateral and you’ll be managing two mortgages at once. You’re taking out another mortgage on your home when you’re borrowing against your home equity. If you neglect to repay either loan, you’re putting your home at risk of foreclosure. By unlocking up to 95% of your home’s equity, you can pay off more debt than other lenders only offering up to 80%.

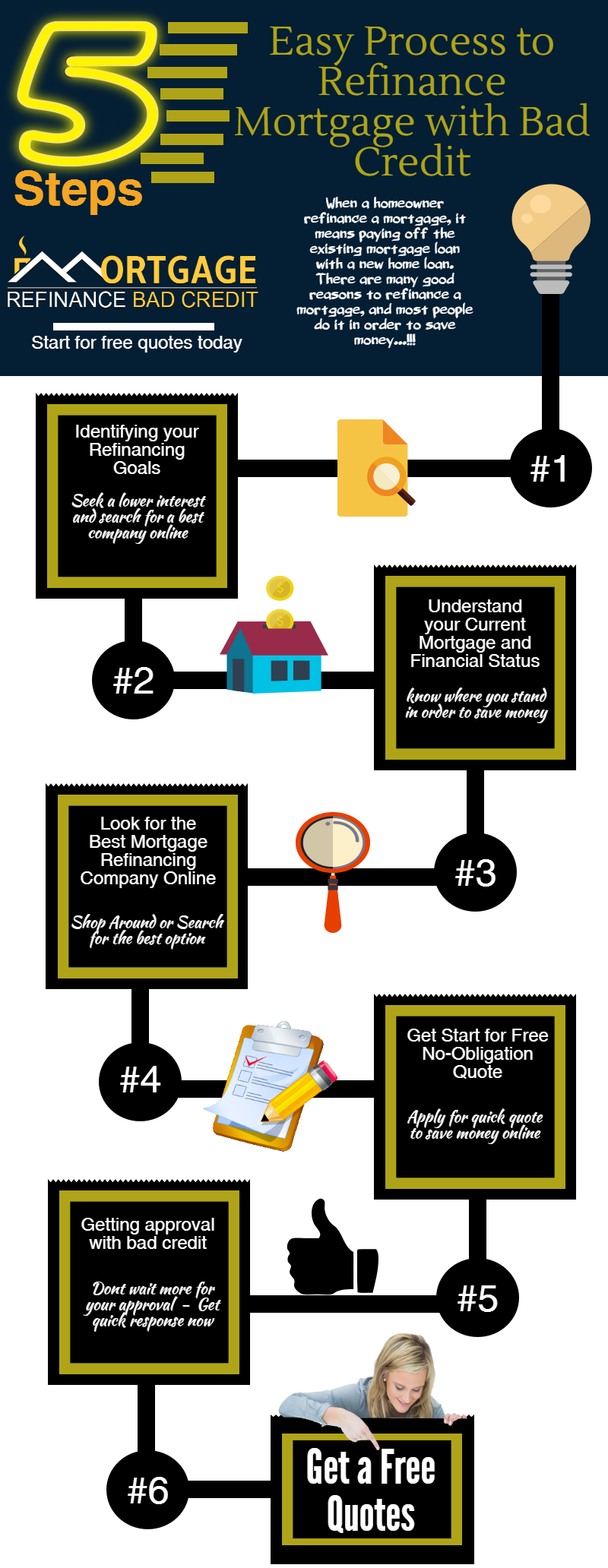

In a standard refinance, you take out a new loan that replaces your original mortgage. There are different types of refinances—from lowering your rate or changing your term to taking cash out. In almost all cases, you'll have just one loan.

Generally speaking, you may borrow against your home if you have built at least 15% equity. LendingTree is compensated by companies on this site and this compensation may impact how and where offers appears on this site . LendingTree does not include all lenders, savings products, or loan options available in the marketplace. LendingTree is compensated by companies on this site and this compensation may impact how and where offers appear on this site . Property insurance is required; if the collateral is determined to be in an area having special flood hazards, flood insurance will be required as well. Lower home equity line of credit annual percentage rate is variable and is based on the value of an index plus a margin.

Because most credit cards have a variable interest rate, they can be riskier than fixed-rate loans. The good news, however, is that you only pay interest on what you borrow and can reuse that available credit once it’s repaid. Watch out for annual fees and other account-related charges, though. Rates, terms, and qualifying details not applicable to stand-alone HELOC options. A HELOC combination product is a combination transaction of refinancing your existing mortgage at the same time as obtaining a subordinate HELOC loan.

We do not assume responsibility for the accuracy, completeness, or timeliness of the information contained therein. Visitors to any linked websites should not use or rely on the information contained therein until they have consulted with an independent financial professional. Please click “I understand” to utilize these sharing features. A Value Home Equity Loan lets you leverage more of the equity you’ve invested in your home by enabling you to borrow much more of your home’s value (up to 95%). Your savings are federally insured to at least $250,000 and backed by the full faith and credit of the United States Government. Meet with Financial Consultants who can recommend a mix of quality investment options, such as mutual funds, IRAs and fixed annuities, based on your unique situation.

Please be aware that this is not an advertisement for credit. Nothing on this site contains an offer to make a specific home loan for any purpose with any specific terms. This is a web-site and no loans can be guaranteed as loans and rates are subject to change. AmeriChoice recently started offering home equity loans for 100% loan-to-value.

It’s a second loan secured by your equity in the house—the current value of the property minus what you still owe. Unless your home is paid for, you’ll have two payments to make. But, depending on the amount you borrow, your HELOC payment can be very low. Even if you’re approved for a large amount of credit, you’ll only be paying on the funds that you actually borrow. If you own a home, you should do yourself a favor and consider a 2nd mortgage next time you need money and want to make the best financial decision.

No comments:

Post a Comment